Blog Post: Promoting Efficiency Through Sensible Defaults—The Power of Automated Enrollment in Retirement Savings

At the Institute for Responsive Government, we’re always looking for policy solutions that make government more efficient, accessible, and responsive to the needs of real human beings. One way governments can do this is by employing “Nudge Theory,” a concept of behavioral economics that encourages the use of thoughtful design choices — called “nudges” — to ensure that people can easily locate and select the most commonly preferred option.

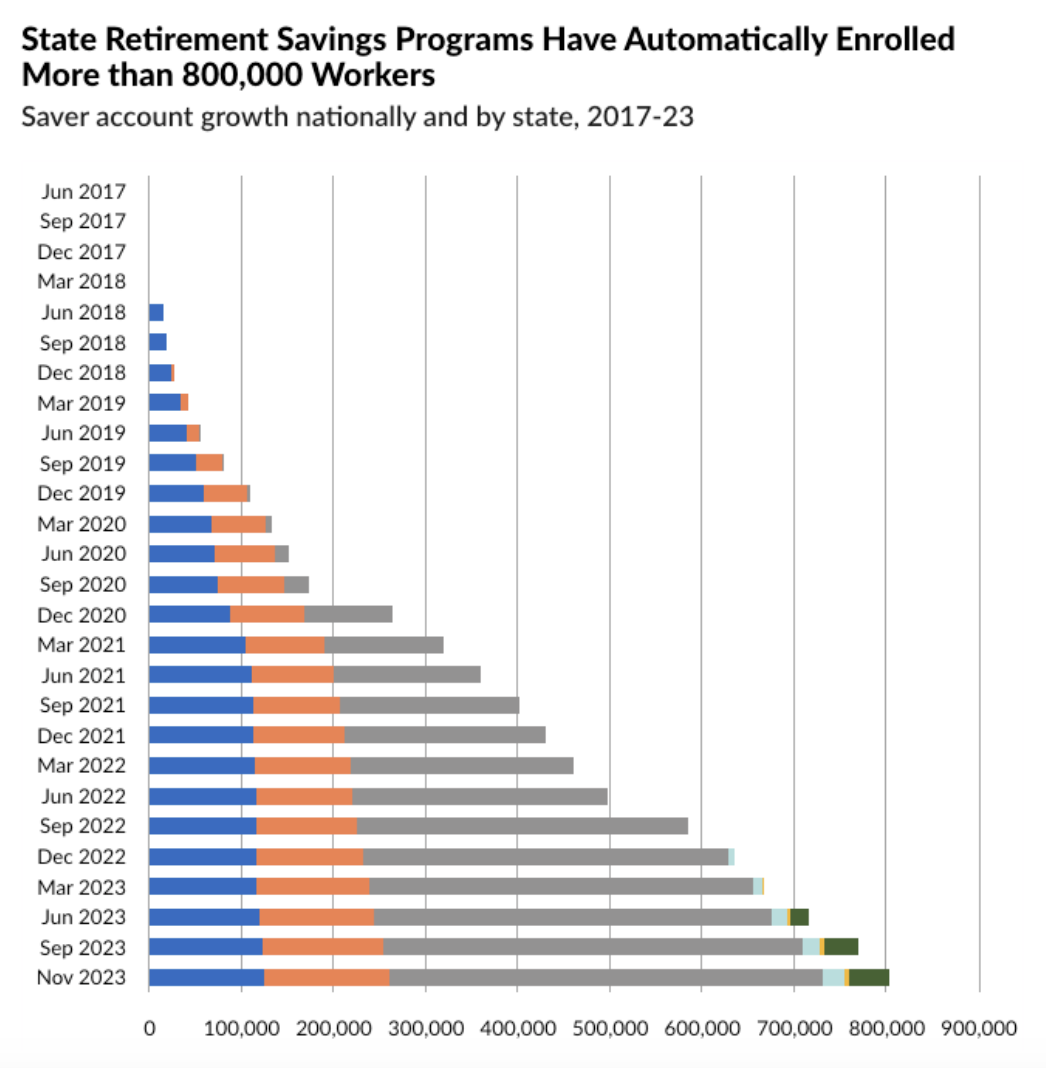

One striking example of the power of defaults lies in the realm of retirement savings, where switching the default from opt-in to opt-out has proven to be a game-changer in promoting financial security for millions. American workers are 15 times more likely to save if they can save at work through an automatic payroll deduction. Traditionally, many retirement savings plans required individuals to actively opt in by taking deliberate action to enroll in the plan (read: filling out paperwork). Like in the voter registration context, the opt-in default led to inertia — it turns out it’s less a story about individuals deciding not to save for retirement and more about individuals not being willing to navigate daunting levels of red tape.

Enter automated enrollment — a simple yet ingenious solution that switches the default option from “not saving” to “saving.” Automatic enrollment programs accomplish this through two mechanisms. First, they automatically enroll workers in the savings program. Second, they automatically deduct a set contribution from each paycheck. Workers remain free to adjust their enrollment or their payroll contributions according to their own desires or needs.

The switch from opt-in to opt-out enrollment has yielded remarkable results across the seven states who have implemented the switch. In addition to greatly expanding the overall number of workers enrolled in savings programs, the pool of users has looped in a diverse crowd of younger, female, unmarried workers who have been more likely to be left out of traditional opt-in programs, according to Pew Research.[1]

Six more states plan to implement automatic savings programs in the next two years.[2] A number of states are considering legislative proposals during their 2024 sessions (Georgetown’s Center for Retirement Initiatives tracks them here).

Automated enrollment in retirement savings plans stands as a shining example of harnessing the power of defaults to make the government more responsive to the needs of real human beings. Saving for retirement and not saving for retirement are both choices — but an opt-out system recognizes that most people want to save, so it makes the majority preference the easiest choice. We like it when system design choices align with the preferences of the majority.

As we continue to explore innovative ways to make government work better for real people, the switch to opt-out savings enrollment is a compelling case study in the transformative power of simple yet effective policy solutions.

[1] The seven programs are OregonSaves (2017), Illinois Secure Choice (2018), CalSavers (2019), MyCTSavings (2022), Maryland$aves (2022), Colorado SecureSavings (2023), and RetirePath Virginia (2023).

[2]Maine, Delaware, Hawaii, New Jersey, New York, and Vermont, all plan to go live by 2025 at the latest.